What Is a Liquidity Pool? Solana LP, Depth and Impermanent Loss

What a liquidity pool is and how to read one on Solana: pool depth versus TVL, slippage math, impermanent loss and concentrated ranges, with worked examples.

Most people guess at liquidity. They look at a Solana liquidity pool, see a big number, and assume their swap will go through clean. Then they push 5,000 USDC at a small token, watch the price move 8 percent against them, and learn the hard way that a pool's headline value has very little to do with how much actual room it gives a trader.

Liquidity is that room. It answers a single question: how much can I move in or out before the price refuses to play along? On Solana that question has a real, calculable answer, and the math is friendlier than it looks.

This guide walks through the concept in plain English, the four numbers that actually describe a pool, why AMMs (automated market makers, self-running trading pools) behave the way they do, and the practical decisions an LP and a trader make from the same numbers. The point is intuition, not memorization.

1. What a liquidity pool actually is

Short version: liquidity is the ability to swap one asset for another quickly, at a fair price, without moving that price. Picture a small currency exchange booth. The rate on the window looks great, but if the booth only has 300 dollars in cash and you walk in wanting to change 5,000, the clerk will tilt the rate against you. A thin market behaves exactly the same way.

Another picture: a grocery shelf. If there are three cartons of milk left, taking the second one barely moves anything, but the third sale forces the manager to restock at a higher cost. A shelf overflowing with stock absorbs your purchase without flinching. Pool depth is that shelf.

In traditional markets you measure liquidity through bid-ask spread and order book depth. DeFi rewrote that. There is no classic order book on Raydium or Orca. There is a pool. The pool holds two assets, and a simple math rule decides what comes out for what goes in. The deeper the pool, the less the rule bites you. The shallower the pool, the more it owns you.

On Solana you will run into two main flavors:

- Uniform pools. Money is spread evenly across every price. Raydium standard pools, classic Meteora pools, Orca's older pools, PumpSwap. Simple, easy to understand, but they need a lot of capital to feel deep.

- Concentrated pools. Liquidity is packed into a chosen price range. Raydium CLMM, Orca Whirlpool, Meteora DLMM. The same idea, different math, much tighter execution inside the range, with a catch when price wanders outside it.

Liquidity is not the money in the pool. It is how much price movement that money buys you for a given trade size. A $10M pool with a thin live range can be tighter than a $1M pool with a wide one.

2. The four numbers that describe a pool

If you remember nothing else, remember these four. They are the lens through which every Solana DEX dashboard makes sense.

a. Total value in the pool (TVL)

The combined dollar value of both sides of the pool. In an example SOL/USDC pool, if SOL trades at $92.61 and the pool holds 1,000 SOL plus 92,610 USDC, each side is worth $92,610 and the total is about $185k.

TVL is a flat number. It tells you the pool exists and how big it is. It tells you nothing about how that money is spread across price levels, and that distribution is what determines whether your trade clears cleanly.

b. Pool depth

The largest trade you can make at a given slippage tolerance. The standard reference desks quote each other is "depth at 1 percent slippage."

For the example pool above, if you are willing to accept 1 percent slippage, you can swap roughly $925. Want to push $10,000 through the same pool? Expect closer to 9 or 10 percent slippage. The pool does not care that its TVL says $185k. It only cares about keeping the ratio between its two sides intact.

c. Slippage and price impact

Slippage is the gap between the price quoted on your screen and the price your trade actually executed at. Price impact is the same thing viewed from the other side: how much your trade alone moved the pool's mid-price.

Take the same pool, three different trade sizes. A $100 swap nudges the price about a tenth of a percent. A $1,000 swap moves it about 1 percent. A $10,000 swap moves it 9 percent.

| Trade size (USDC) | Quoted SOL | Actual SOL | Slippage |

|---|---|---|---|

| 100 | 1.0800 | 1.0790 | 0.10% |

| 1,000 | 10.8000 | 10.6900 | 1.06% |

| 10,000 | 108.0000 | 98.9000 | 9.10% |

Notice the curve. Doubling your trade size does not double your slippage. It compounds. Splitting a large order into smaller pieces over time is a real strategy because of this, not a meme.

d. Daily volume divided by TVL

The single healthiest signal for "is this pool actually used." Take 24-hour volume, divide by TVL. A ratio above 0.5 means the pool turns over often, spreads stay tight, and arbitrage traders keep the price honest. A ratio below 0.05 means the pool is parked capital nobody is touching, and the price you see may be hours stale.

Pools with high TVL and low volume ratios are a classic LP trap. The yield looks attractive on paper, the price swings still hurt you, and the fees never catch up.

3. How pools actually price your swap

Let's explain the formula without turning it into a math class. Picture the pool as a seesaw. SOL on one side, USDC on the other. The pool's job is to keep one rule alive: the product of the two sides has to stay constant. So if you pile money onto the USDC side, the SOL side has to release enough SOL to keep that product the same.

Back to the example: 1,000 SOL and 92,610 USDC. A trader pushes 1,000 USDC into the pool. The USDC side rises to 93,610. To keep the original product intact, the pool releases about 10.69 SOL out of the SOL side. That is what the trader walks away with.

The market price before the trade was $92.61 per SOL. The price the trader actually paid was $1,000 divided by 10.69 SOL, which works out to about $93.55 per SOL. That gap of roughly 1 percent is the slippage.

This is why bigger trades hurt more. The more you unbalance the seesaw, the harder the rule pushes the price against you. The pool has no opinion. It just enforces its rule.

4. Concentrated pools change the rules

In a concentrated pool the LP says: "I will provide liquidity only between price A and price B." Inside that range they collect full fees. Outside it, the position holds 100 percent of one asset and earns nothing until price wanders back.

The efficiency win is large. With SOL trading around $92-93, a concentrated $100k position pinned to the $90-$95 band feels 10 to 50 times tighter than a uniform $100k pool, because all the money is bunched right where trades happen. The downside is just as clean: stepping out of range turns the position into a directional bet you did not sign up for.

| Range width | Fee capture | Price swing exposure | Out-of-range risk |

|---|---|---|---|

| Very narrow (±2%) | Highest | Highest | Constant rebalancing |

| Moderate (±10%) | Strong | Moderate | Manageable |

| Wide (±50%) | Modest | Mild | Rare |

| Full range | Same as uniform pool | Same as uniform pool | Never |

If you are starting out, wide ranges are forgiving. If you are running an active position, narrow ranges with a rebalance plan beat passive ones, but only if you actually rebalance. A narrow range nobody touches is the worst of both worlds.

5. Impermanent loss, in plain English

Impermanent loss is the gap between holding two assets in a pool and just holding them in your wallet. The name is misleading because it is not really a loss, it is a comparison. No money vanishes from the pool. It is just that when the price moves, sitting in a pool gives you a different result than sitting in a wallet.

The mechanic is simple. The pool has to keep its two sides in balance. When SOL goes up, the pool automatically sells some SOL and takes in USDC, so you end up with less of the asset that mattered. When it drops, the reverse happens. If you had just held, the rising asset would still be there in full.

| Price change | Gap versus just holding |

|---|---|

| +25% | −0.6% |

| +50% | −2.0% |

| 2x (+100%) | −5.7% |

| 3x | −13.4% |

| 4x | −20.0% |

| 5x | −25.5% |

Impermanent loss is not a loss against your entry. It is a gap against the simple hold alternative. A pool that paid you 12 percent in fees during a 2x move on the asset still left you with about 6 percent net versus holding. Whether that is a win depends entirely on the fees, not on the IL number alone.

The honest LP question is never "what is my impermanent loss." It is "did fees and rewards beat the gap given how much the price actually moved." Inside a tight concentrated range, fees usually win by a wide margin if the price respects the range. On a volatile asset in a wide passive position, fees usually lose.

6. Reading what your LP position is worth

Uniform pools hand you a ticket (an LP token) that represents your share of the pool. The value of the position is a simple ratio. If the pool's total value is $500k and your tickets represent 1.5 percent of the supply, your position is worth $7,500 right now, split across both assets at the pool's current ratio. Add accrued fees, subtract the gap versus holding, and you have your real return.

Concentrated positions skip the ticket. Each position is an NFT with its own range and amount of money. The logic is the same in spirit (your share, your fees, your gap) but the panel already breaks it down. The practical work is reading the breakdown rather than computing it.

7. Picking a Solana liquidity pool: a quick checklist

If you are deciding where to provide liquidity or where to route a trade, run the candidates through this set of filters:

| Check | Pass | Fail |

|---|---|---|

| TVL for active use | Above $500k | Below $100k means high slippage even on small trades |

| Volume / TVL ratio | Above 0.5 daily | Below 0.05 means the pool is parked, not traded |

| Fee tier match | 0.30% for volatile pairs, 0.05% for stables, 1% for long-tail | 0.30% on a stable pair will lose to a 0.05% competitor pool |

| Range positioning (concentrated) | Range covers the realistic 7-day price band | Range too tight without a rebalance plan |

| Concentration | Top 5 LPs hold less than 50% | Whale-dominated pools rug their own depth on exit |

On fee tiers: a stablecoin pair (USDC/USDT) sitting at 0.30 percent is leaving most of its volume to the 0.05 tier next door. A small-cap token at 0.30 percent with no 1 percent option is underselling its own volatility. The fee tier is part of the pool's product positioning, not a small detail.

8. Doing the actual work on J Tools

The numbers above tell you whether to act. The action itself runs through a handful of dedicated screens.

If you want to ship a token and seed real volume in the same operation, the create pool and first buy in one transaction tool bundles both into a single package. That matters because two separate transactions give a sniper bot a free shot at the gap between them.

For an existing pool you already have a position in, the add and remove liquidity screen handles both deposit and withdrawal on Raydium and Meteora pools without bouncing across multiple DEX UIs.

Before any of those, sections 2 and 3 say you should test the slippage curve at the trade sizes you actually plan to run. The batch swap planner across multiple pools lets you stage a sequence of swaps at different sizes and see the realized slippage before committing real capital. Treat it as a depth probe, not just an execution tool.

For LPs who also want to see who else holds positions in a pool before committing, the holder snapshot tool that reads pool participant balances exports the full list in one pass.

9. Common mistakes

- Reading TVL as liquidity. A $10M pool with a wide concentrated range can be thinner around the current price than a $1M pool with a tight range. Always check depth at your trade size.

- Reading the gap as a loss. Impermanent loss is a comparison against just holding, not against your entry. The right question is whether fees and rewards beat the gap given the price move.

- Treating tight concentrated ranges as low risk. A 2 percent range gives the highest fees and the worst out-of-range outcomes. It is high-touch by design. If you cannot babysit it, do not pick it.

- Ignoring the volume ratio. A high-TVL pool nobody trades is parked capital. The yield will not show up because the volume is not there to generate fees.

Before any LP decision, write down two numbers: the realistic 30-day price range, and the daily volume you expect. Pick a pool whose fee tier and concentration match both. If you cannot fill in either number, you are not ready to LP that asset yet.

10. The shorter version

Liquidity is not money, it is room. The four numbers (TVL, depth, slippage, volume ratio) tell you how much room a pool gives you. The seesaw rule behind every pool says exactly how that room shrinks as your trade gets bigger. Concentrated pools buy you efficiency at the cost of needing a view on price. Impermanent loss is real, but it is a comparison, not a loss against entry.

Run the numbers before you commit capital, on either side of the trade. They do not lie, and they are easy enough to do on a phone. For more on the broader DeFi mechanics, the guides category covers tooling and strategy writeups at the same level of depth, and the Solana-tagged archive groups every chain-specific piece in one place.

How to calculate liquidity, step by step

The sections above scatter the math across worked examples. Here is the same work as one short procedure you can run on any Solana pool with the two reserve numbers and the current price.

- Read the two reserves. Every uniform pool holds two amounts, for example 1,000 SOL and 92,610 USDC. The DEX page shows both.

- Find the constant. Multiply the reserves: 1,000 × 92,610 = 92,610,000. This product stays fixed through any swap, which is the rule that prices your trade.

- Value the pool (TVL). Price each side in dollars and add them. With SOL near $92.61, both sides are worth about $92,610, so TVL is roughly $185k.

- Simulate your trade. Add your input to one reserve, then divide the constant by that new amount to get the other reserve after the swap. The difference is what you receive. Push 1,000 USDC in and the SOL side drops to about 989.31, so you get roughly 10.69 SOL out.

- Read the slippage. Compare your effective price ($1,000 ÷ 10.69 ≈ $93.55) to the starting price ($92.61). The gap, about 1 percent here, is your slippage.

Liquidity is not the result of step 3. It is what step 4 reveals: how much you can move before step 5 turns ugly. A pool with a huge TVL but a thin live range will fail step 4 at a smaller size than its headline number suggests. For concentrated pools the same five steps apply, except the constant only governs the active price band, so depth is measured against the liquidity sitting in range rather than the whole position.

Doing this by hand once is worth it for the intuition. After that, stage the trade sizes you actually plan to run and let a tool report the realized slippage instead of trusting the quote on screen.

What is a liquidity pool in crypto?

A liquidity pool is a smart contract that holds a reserve of two tokens and lets anyone swap between them against that reserve, with no buyer or seller on the other side. There is no order book and no counterparty waiting to match you. You trade against the pool itself, and the constant product rule from the section above decides the rate.

The tokens come from liquidity providers (LPs), who deposit both sides in the pool's current ratio. In return they earn a cut of every swap fee, proportional to their share. On Solana the same idea powers Raydium, Orca, Meteora, and PumpSwap, with two structural styles: uniform pools that spread deposits across all prices, and concentrated pools that let an LP pack capital into a chosen band. When you create a new pool you are the first LP, which means you also set the opening price by choosing the ratio of the two deposits. Get that ratio wrong and arbitrage bots correct it for you in the first block, at your expense. If you want to create a liquidity pool or seed an existing one, the deposit screens handle the ratio math so the opening price lands where you intend. Once you hold positions, view your LP positions in one place to track share, fees, and current value without opening each DEX separately.

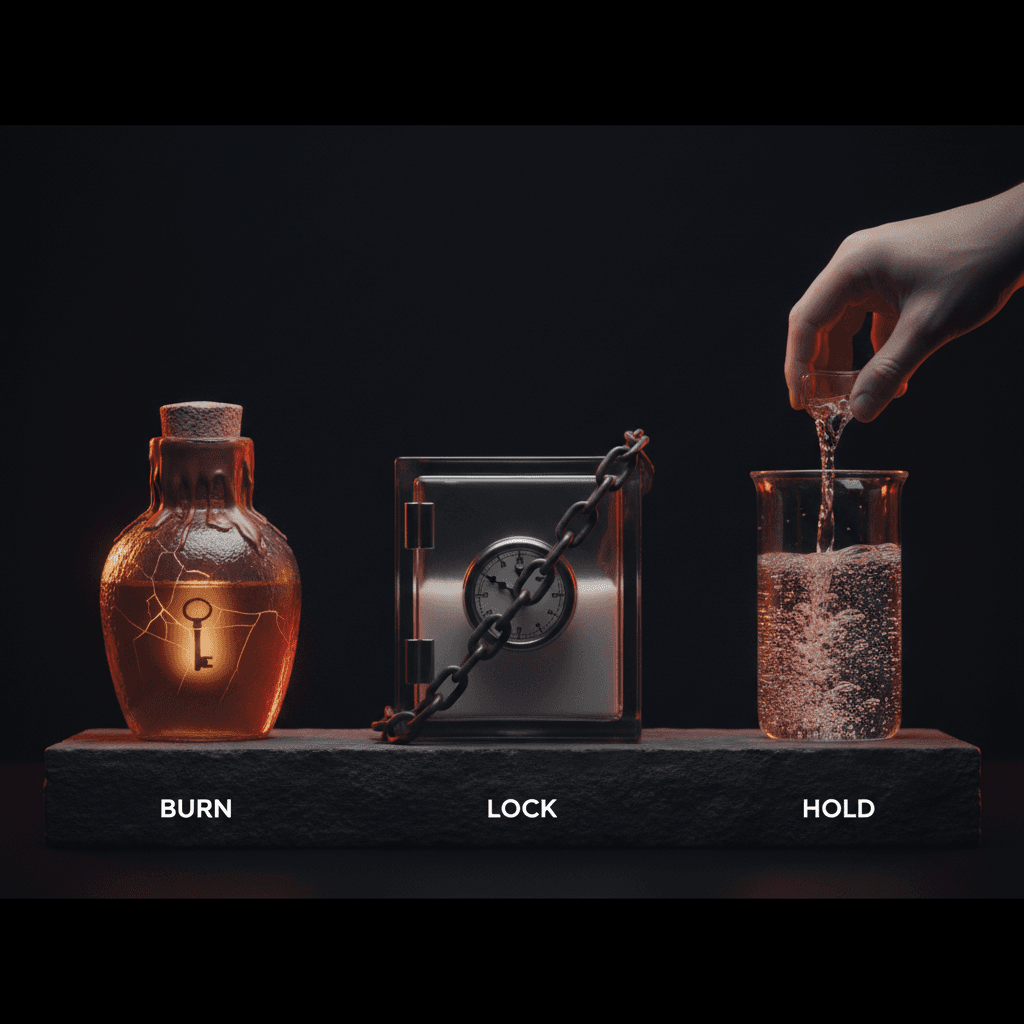

Locked, burned, and exit liquidity

These three phrases come up constantly in token safety chatter, and they describe very different things.

- Locked liquidity means the LP tokens (the receipt for a pool deposit) are held in a time-lock contract the creator cannot touch until a set date. The liquidity still exists and still earns fees; it just cannot be pulled early. A lock reduces, but does not erase, rug risk, because a creator can still dump their own token supply even while liquidity is locked.

- Burned liquidity means the LP tokens were sent to an address nobody controls, so the deposit can never be withdrawn by anyone, ever. This is stronger than a lock. The tradeoff is that the creator also gives up their own fee claim and the ability to migrate the pool. Burned liquidity is a one-way commitment.

- Exit liquidity is not a safety feature at all. It is what late buyers become when a project's insiders sell into them. If a pool is thin and a few wallets hold most of the supply, every new buyer is providing the cash those wallets exit through. The pool-picking checklist above flags this: when the top few LPs hold most of the depth, they can pull it on the way out and leave everyone else holding a price with no room beneath it.

Before trusting any of these claims, verify them on chain rather than taking a tweet at face value. Check who holds the LP tokens, whether they sit in a known lock or burn address, and how concentrated the underlying token supply is. A holder snapshot of the token reads the participant balances directly so you can see concentration for yourself. And once you know depth is real, it is still worth a quick check to check slippage before you swap at the size you actually plan to trade.