Solana Token Burn Strategy: Deep Mechanics and Anti-Patterns

Operator-level Solana token burn strategy guide. Honeypot taxonomy, chart mechanics, verification checklist, and the right tool for each burn type.

Every Solana cycle produces the same announcement, dressed in slightly different fonts. Team burns 5% of supply. Deflationary forever. Buy now. The token pumps for six hours, gives it all back in twenty-four, and the chat moves on. Anyone who has launched more than a handful of tokens knows the pattern. What most operators do not know is why the price acts that way, and which "burns" are actually burns at all.

A burn on Solana is mechanically trivial. Picture throwing a stack of cash into a fireplace, on purpose, with witnesses watching. It is gone, everyone saw it, no recovery. That is what happens on chain. A balance in one wallet drops, and the token's total supply drops by the same amount in the same step. The protocol holds no opinion about whether the act is economically meaningful, deceptive, or theater. That judgement is yours, and most operators get it wrong because the language around burns has drifted far from what the chain actually does.

This post is for the operator side of the desk. Token managers, market makers, protocol designers. The aim is to surface what a Solana solana token burn strategy actually buys you, where the honeypot patterns hide, and how chart mechanics betray the difference between a legitimate burn and a press release.

The supply illusion

The first trap is conflating circulating supply with total supply. On Solana these are two different numbers, sourced from two different places, and only one of them is verifiable on chain in a single read.

Total supply lives on the token's central record page; anyone can fetch it. Circulating supply is a CoinGecko or CoinMarketCap convention, computed by subtracting wallets the issuer has tagged "non-circulating" (team, treasury, vesting). When a project announces we burned 5% of circulating supply, on-chain total supply may not have moved at all. The team burned tokens already off-circulating, or burned from a treasury and reported it as a circulating reduction, or burned and re-minted the same week using a live new-issuance authority.

The honest test fits in one sentence. Did total supply drop, and is the new-issuance authority revoked? If both, the burn is real and final. If either fails, you are looking at marketing.

The single highest-signal field on any Solana token claiming deflation is the new-issuance authority. If it is still assigned, any burn is reversible by the authority holder. Someone burns a million tokens today, the same person prints a million the next day, and you are right back where you started. Solscan shows this on the token page; you have no excuse for missing it.

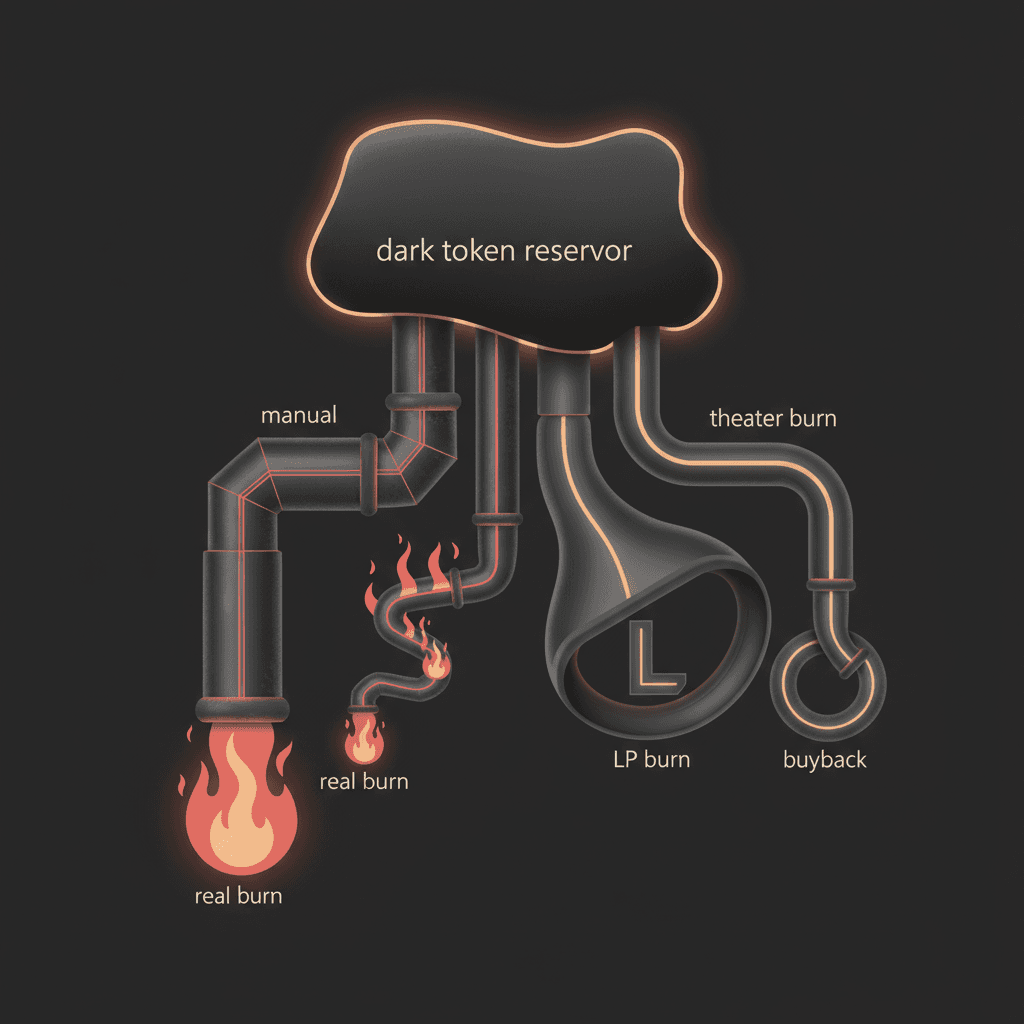

Burn types, decomposed by economic signal

Five burn mechanics exist on Solana in practice. They look similar on a chart but carry different signal strength.

Manual one-time burn. Operator signs a burn from their wallet once, supply drops. Highest immediate signal because it is visible and final. Lowest long-term signal because nothing repeats. Think of a company publicly shredding a stack of stock certificates at an announced event. Everyone left holding shares owns a slightly bigger slice of the same business.

Scheduled treasury burn. Project commits to quarterly burns from treasury. Trust depends on the operator following through. BONK has run community burns of around one billion tokens every quarter, which is roughly a company publicly shredding 1% of its stock; remaining holders own slightly more of the total. Chart impact is real but small; the brand impact is the product.

Revenue-funded buyback and burn. Protocol earns fees in SOL or USDC, market-buys the project token, then burns. The cleanest mechanism economically because the demand side is genuine. Jupiter's buyback program is the reference for how to publish this credibly.

Programmatic transfer-fee burn. The Token-2022 transfer fee extension taxes every transfer in basis points. An automated harvester routes accumulated fees to a burn address. Highest trust mechanic if the recipient is verifiably a burn destination, zero trust if the recipient is a team-controlled wallet.

Liquidity pool receipt burn. Operator sends the receipt tokens of the primary Raydium or Meteora pool to a burn address, removing the ability for anyone (including the team) to withdraw the paired liquidity. A different animal: it does not burn supply, it burns the operator's exit. Markets read it correctly as a commitment device.

The mechanism a project chooses should match the story it wants to tell, and the story should match actual cash flows.

What burns actually do to charts

Per-token math is where most analyses stop and where most analyses go wrong. Burning one percent of supply changes the theoretical share per token by a factor of 1.01. In practice, price is set by the marginal buyer, not by supply division. A 1% burn moves the per-token claim by rounding error. What it moves is sentiment, and sentiment expires fast.

Observable Solana pattern from 2024 through early 2026: a burn announcement on a mid-cap token (fully diluted value of 20 million to 500 million dollars) produces an immediate spike of 8% to 25% in the first hour, followed by a sell-off erasing most of the gain within 24 hours. Three forces drive it. Insiders front-run with two to seven days of accumulation. Post-announcement traders take profit. Sophisticated holders realize the burn is small relative to live circulating amount and rotate.

Liquidity depth is the more interesting story and the one operators do not model. If burned tokens come from inside the pool, the paired SOL or USDC leaves the pool too. A 10% reduction of the token side of the pool can take slippage on a $10k buy from 2% to 11% or worse, depending on curve and starting depth. Operators who burn pool positions for optics rarely model what it does to subsequent volume.

Burning tokens held in a Raydium pool position reduces supply and pool depth on both sides of the pair at the same time. Run a slippage simulation at $1k, $10k, and $100k notional before and after, and only burn if the post-burn depth is still livable. If the post-burn buyer pays 11% on a small order, no deflation headline rescues them.

The third chart mechanic is aggregator behavior on Token-2022 transfer fees. Jupiter incorporates fee-on-transfer pricing when metadata is indexed correctly, but the routing layer widens quotes to absorb the fee and slippage tolerance degrades fast. Some routes silently skip Token-2022 tokens with non-zero transfer fees because the math breaks the standard atomic-swap assumption. A token marketing "automatic deflation" through transfer fees can quietly lose the routes that make it tradable.

Honeypot taxonomy

This is the meat of the post. Each pattern below has been observed in the wild on Solana since the 2024 cycle. Names are mine; the mechanics are the point.

Authority-kept burn theater. Project burns 5% of float and announces deflation while the new-issuance authority is still live. A buyer who reads the token's record page sees the authority address and knows the burn is cosmetic; the same supply can return on the next signature. The fix: operators revoke the new-issuance authority publicly in the same week as the burn, on chain, in one verifiable step. If a team will not, the burn is not the story; the live issuance authority is.

Vesting-supplanted burn. Team announces a 2% burn on a Monday. On the Friday of the same week, a vesting cliff unlocks 6%. Net circulating supply is up. The burn was real; the headline was honest in isolation; the combined effect is opposite to what the announcement implied. Anyone who reads the vesting schedule alongside the burn calendar spots it in five minutes. Almost nobody does.

Permanent delegate quiet burn. Token-2022 supports a permanent delegate extension. Once set, the delegate can move or burn from any holder's balance without their signature. Projects market this as "anti-bot deflation" and the public version is sometimes legitimate. The honeypot version uses it to burn from wallets the team has decided are dumpers. It is a polite on-chain confiscation, and most holders never check whether the token they own carries this extension.

Fake pool burn. Operator burns pool receipt tokens from a satellite wallet holding 0.2% of the real pool position. The primary position, in a different wallet, stays live and withdrawable. Solscan shows the burn. CoinMarketCap may flag the project as "LP burned" for 24 to 72 hours before someone notices. Verification: read the pool receipt's record page, find its largest holder, confirm the address is a known burn destination.

Buyback funded from project treasury. Team uses USDC raised in the ICO to "buy back and burn" the same token. The buy prints upward, the burn produces a deflation headline, but the demand is the team's own capital looping back. Net effect on price discovery is near zero. Real buyback programs are funded by external revenue (DEX fees, protocol revenue, marketplace cuts) and publish the source.

Transfer-fee recipient never burns. Token-2022 token with a 1% transfer fee. Fees accrue to a wallet labeled "burn destination." The wallet operator routes balances to liquidity removal or over-the-counter dumps rather than burning. Holders see fees collecting and assume burn; nobody audits the destination outflows. The fix: set the fee recipient to a verifiable burn address (the standard incinerator address) or to a program that only allows a burn step.

Graduation burn with parked supply. Pump.fun-style launches promise a pool receipt burn at Raydium graduation. The burn does happen. Meanwhile the operator has accumulated supply in satellite wallets during the bonding-curve phase. Post-graduation, the parked supply enters the market over weeks. The pool burn looks like commitment; the satellite stack keeps the operator in control of circulating supply.

Two flags catch most of these without any deep analysis. The new-issuance authority must be revoked. The largest holders after the issuer should not be wallets created within a week of launch. If either fails, the deflation claim is unverified.

Verification checklist for buyers

Five reads on Solscan separate a real burn from theater. Each takes under two minutes.

- Open the token's record page. Confirm that the new-issuance authority and the freeze authority are revoked. If either is set, the burn is not final.

- Pull total supply before and after the announced burn. The delta should match the announced amount within rounding.

- Check the top 20 holders. Identify wallets created in the same week as launch. Cluster the ones moving in lockstep; that is the operator's parked circulating supply.

- For Token-2022 tokens, list extensions. Audit where the transfer fee recipient sits, confirm the permanent delegate field is empty or assigned to a known program, and watch for default-frozen account state (a separate trap).

- For pool burns, fetch the pool receipt's record page, identify its top holders, and confirm a burn address holds the supply you expected. Cross-check on Raydium directly, not Birdeye or CMC.

Operators serious about a deflation story publish exactly these numbers in their docs, with on-chain links.

Fixed, deflationary, or mintable: choosing the supply model

The burn strategy above only matters once the supply model underneath it is set. That choice happens before launch, and it decides whether burns are even the right lever. Three models cover almost every real token.

Fixed supply mints everything once, then revokes the new-issuance authority so the cap can never grow. This is the Bitcoin-style floor and the default for memecoins, where scarcity is the whole pitch. Deflationary supply starts fixed and shrinks over time through burns or a Token-2022 transfer fee that routes to a burn address. Mintable supply keeps the issuance authority live on purpose, because the token has to print more later.

| Project type | Best fit | Why |

|---|---|---|

| Memecoin or community token | Fixed | Scarcity is the entire pitch. Revoke mint and freeze at launch. |

| Gaming or utility token with real volume | Deflationary (Token-2022 fee + burn) | Fees turn usage into scarcity without a manual vote. |

| Stablecoin or wrapped asset | Mintable (multi-sig or program) | Supply has to track off-chain reserves. |

| Governance token with staking | Mintable (program-controlled) | Emissions need a live, rule-bound authority. |

| Loyalty or points token | Mintable (issuer wallet) | The issuer prints on user action. |

A label in a whitepaper proves none of this. A token is deflationary because a burn instruction or a fee rule enforces it on chain, and fixed because the issuance authority is gone. That is the only scarcity a buyer can verify. Lock a fixed cap with the revoke mint authority tool, and run any supply reduction through the burn tokens tool.

Strategy taxonomy for honest operators

Different burn mechanics serve different goals. The table below is the one I would put on the whiteboard before deciding.

| Mechanism | Economic signal | Automation | Governance overhead | Trust signal |

|---|---|---|---|---|

| One-time strategic burn | High at moment, low after | Manual | None | Strong if issuance authority is revoked afterwards |

| Scheduled treasury burn | Medium, repeats | Manual cadence | Treasury policy needed | Depends on follow-through |

| Revenue-funded buyback and burn | High and ongoing | Semi-automated | Revenue tracking | Strongest when source is external |

| Programmatic transfer-fee burn | Continuous, small per transaction | Fully automated | None after launch | Strong if recipient is a burn address |

| Pool receipt burn | One-time, commitment | Manual | None | Strong if the burned position is the primary one |

A solid solana token burn strategy usually pairs two mechanics. A typical pattern: launch with fixed supply and immediate revoke of the new-issuance authority, then add a revenue-funded quarterly buyback once cash flow exists. The first kills dilution risk; the second adds a real demand mechanic. Memecoins skip the second and run on one-time burns plus narrative, which is fine as long as nobody pretends the burns are doing more than they are.

For a deeper read on whether fixed, deflationary, or mintable is the right floor for your token, see the token supply strategy guide. For the authority side of the same decision, the revoke authority guide walks through what each authority controls and when to drop each one.

Burn versus revoke mint authority: the 2x2 buyers actually read

These two actions get mixed up constantly, and they do opposite jobs. A burn lowers the current supply and cannot touch the future. Revoking the mint authority freezes the future supply and cannot touch what already circulates. The signal a buyer reads comes from the combination, not either one alone.

| State | What buyers see | Real-world example |

|---|---|---|

| Mint live, no burns | Standard mintable token. Solscan shows "mintable: yes". Trust rests on the team's word. | Day-zero memecoin before any cleanup. Most rug candidates sit here. |

| Mint live, burns done | Deflationary illusion. Supply dropped, but the mintable badge is still on and the burner can reprint next block. | A "20% community burn" run for marketing while mint authority stays live. |

| Mint revoked, no burns | Hard-capped at the current level. Supply cannot grow. Listing teams see "mintable: no". | Standard 1B memecoin: mint everything, fund the LP, revoke. |

| Mint revoked, burns done | Locked and reduced. Strongest on-chain deflation signal; supply can only fall from here. | An unsold-ICO burn followed by a revoke. |

The mistakes cluster in predictable places:

- Burning the treasury and assuming the cap is locked. The mintable badge stays on and a fresh batch can print next block. If the goal was "no more inflation", you wanted revoke.

- Revoking before the team allocation is minted. Whatever has not been distributed yet is lost for good. Mint everything, distribute, then revoke.

- Burning from the LP-paired wallet. Tokens sitting inside a Raydium or Meteora pool are pool depth. Burn them and slippage explodes. Always burn from a non-LP wallet.

- Revoking before metadata is final. Lock the cap last, once the name, symbol, and artwork are signed off, or you cannot fix a typo.

Do the burn with the burn tokens tool, then lock the cap with the revoke mint authority tool. Running one without the other leaves the deflation claim half-built.

Executing a burn on j.tools

The j.tools burn tokens tool is a direct burn builder. It does one thing. Paste a token address, an amount or a "burn all balance" flag, sign once with the holding wallet; total supply drops on confirmation. No subscription, no automation, no recipient list. It signs the same burn step the protocol provides, with wallet account derivation and Token-2022 program detection handled inside the tool.

Burn from the operator wallet that actually holds the supply you want to remove. Sending tokens to a "burn address" first costs an extra transaction, leaves a one-block window of exposure, and produces a less clean Solscan trail. Direct sign with the burn tokens tool is the cleaner path.

The adjacent tools fit a typical operator stack. Capture the pre-burn state with the token holder snapshot tool; it files the on-chain read you need to later say "we burned on this date, here is exactly who held what before and after." The revoke mint authority tool is the partner action to any honest burn campaign; running a burn without revoking the issuance authority leaves the deflation claim half-built. The make metadata immutable tool prevents the token's name, symbol, or image from being rewritten after the burn, closing the "let's redefine the asset after we deflate it" escape hatch. After the burn, the small empty wallet accounts left behind hold rent; the close account tool reclaims that locked SOL back to the operator wallet, one account at a time.

For broader context, the Solana guides category covers adjacent topics; Solana tagged posts include the supply-decision and authority-revocation reads you should already have under your belt.

The takeaway

A burn is the cheapest, most legible action a token operator can take. It is also the easiest to fake, because the announcement does the work and the on-chain reality goes unread. Anyone serious about deflation revokes the new-issuance authority in the same week, publishes the source of any treasury funding, and stops conflating circulating with total. Everyone else is running marketing that decays in 24 hours and trains the next cohort of buyers to discount the claim.

If you can describe your burn in one sentence and back every word with a Solscan link, you are running a strategy. Otherwise you are running a press release.

What is a token burn?

A token burn permanently destroys a set amount of a token, and the total supply drops by that exact amount in the same on-chain step. To burn a token means to send it into destruction on purpose, with the transaction visible to anyone. There is no recovery and no recipient who can later spend it. On Solana the burn instruction lives in the token program itself, so the supply field on the mint account decreases the moment the transaction confirms.

This is the plain-English version of the supply mechanics covered above. If you only remember one thing: a real burn lowers total supply on chain, not just a "circulating" figure on a price aggregator. When someone says they burned tokens, the proof is the supply number on the mint's record page going down, nothing else.

How to burn a Solana token (step by step)

The literal flow from your own wallet, no scripts and no private keys handed to anyone:

- Connect the wallet that actually holds the tokens you want to destroy. The burn has to come from the holding wallet, since the protocol decrements that balance directly.

- Open the tool to burn Solana tokens and pick the mint with the token selector. Classic SPL and Token-2022 mints are both detected automatically.

- Enter the amount to burn. Double-check the decimals so you are not burning a thousand times more or less than intended.

- Review the platform fee shown on the tool page (the live amount is displayed there before you sign, since fees change over time).

- Sign the single burn transaction in your wallet. On confirmation, total supply drops by the amount you entered.

- Copy the Solscan link for the transaction. That signature, plus the before/after supply numbers, is your verifiable proof.

Burn straight from the holding wallet instead of sending tokens to a separate "burn address" first. The direct burn is one transaction with a clean Solscan trail, while the two-step route adds an extra transaction and a short window where the tokens still exist in a wallet.

Does burning a token raise its price?

This is the question everyone types into a search bar, so here is the straight answer: not on its own. A burn lowers supply. Price needs demand, and those are two separate things. Fewer coins existing does not create people who want to buy them.

The largest burn in crypto history makes the point. In May 2021, Vitalik Buterin sent roughly 410 trillion SHIB (about 90% of his holdings, near $6.7 billion at the time) to a dead address. That is a Shiba Inu example on Ethereum, not Solana, and it is still the reference every burn story gets measured against. The supply cut was enormous and permanent. The price since then has tracked demand cycles and market mood, not that single event.

BONK is the Solana version worth studying. Its community burns run in large quarterly batches, each a discrete on-chain transaction you can confirm on Solscan. The supply drop is real and verifiable. The chart move around each burn is usually modest and fades fast, because the burned amount is small next to the live circulating supply.

Supply down is not the same as demand up. A burn with no real buyers behind it usually gives back its spike within a day.

Treat "we burned X tokens" as one data point, never as proof a token will rise. A burn grabs attention and can act as a commitment signal. It is not a money machine, and plenty of tokens burn supply while the price keeps falling because demand was never there. Before trusting any deflation claim, check how concentrated the ownership is with the token holder snapshot tool.

Real burn events you can verify

Branded burns are the easiest way to see honest mechanics in practice. The BONK community burns, run in large quarterly batches, are a good reference: each one shows up as a real drop in total supply on chain, and the team publishes the signature so anyone can confirm it on Solscan. Jupiter's buyback program is the cleaner economic model, since the demand side is funded by actual protocol revenue rather than treasury capital looping back on itself.

Use these as the benchmark when you read any new "deflationary" claim. Pull the mint's record page, compare total supply before and after the announced date, and confirm the new-issuance authority is revoked. If a project's burn cannot survive that two-minute check, it is a headline, not a burn.